Selling ESOP Shares in a Secondary Transaction: Tax Implications You Must Plan For

Secondary ESOP sales trigger capital gains tax, advance tax, and FEMA rules. Plan LTCG timing and avoid costly tax mistakes.

Accorp Compliance Team

Our team of compliance experts specializes in PCI DSS, SOC 2, and other security frameworks to help businesses achieve and maintain compliance.

Secondary transactions for ESOP holders in Indian startups have moved from rare to routine. Investors offering employee liquidity windows, founder-led buyback programmes, and VC-facilitated tender offers now give startup employees a real exit path — often years before an IPO.

But selling employee stock ownership shares in a secondary transaction is not as simple as receiving a bank transfer and moving on. Every secondary sale by an ESOP employee triggers a specific, time-sensitive, and often significant tax liability. Employees who do not plan ahead face unexpected advance tax demands, interest penalties under Sections 234B and 234C, and in some cases, a tax bill that consumes most of their gain.

This guide covers exactly what happens when you sell your employee share ownership in a secondary transaction — the tax treatment, the cost rules, the holding period thresholds, the advance tax obligations, and the specific planning moves that can save you meaningful money.

What Is a Secondary Transaction for ESOP Shares?

A secondary transaction is any sale of ESOP stock that occurs outside of a public market — typically before an IPO or acquisition. Common structures include:

Investor-led liquidity windows — incoming investors (at Series B, C, or pre-IPO) offer to buy shares from existing employees as part of the funding round

Tender offers — the company organises a structured buyback process where employees can sell exercised shares back at an agreed price

Direct secondary sales — employees sell to existing investors, new investors, or secondary market platforms with the company's prior written consent

PE / late-stage secondary — private equity buyers acquire blocks of employee shares directly

In all of these cases, the ESOP employee is selling unlisted shares of a private company. This makes the tax treatment categorically different from selling shares on the NSE or BSE.

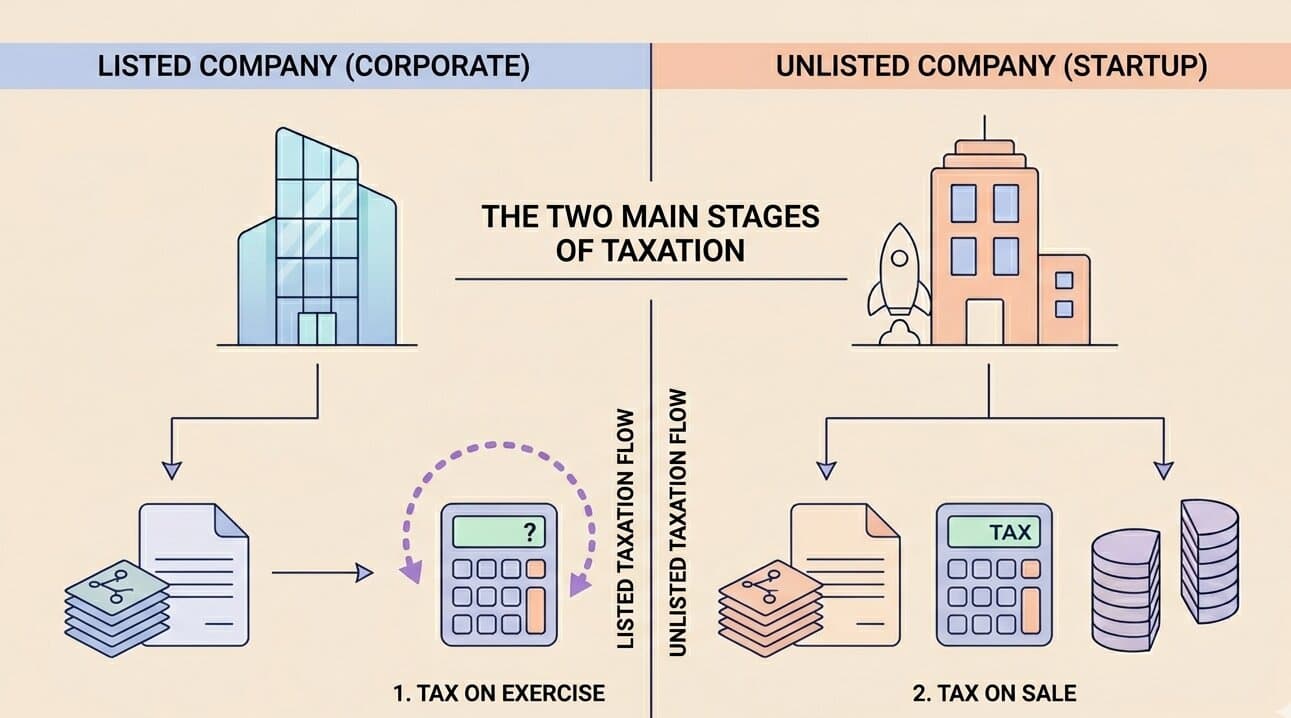

The Two-Stage Tax You Have Already Cleared Before You Sell

Before discussing the secondary sale tax, it is important to be clear about what has already been taxed.

When you exercised your options under your employee stock option plan, the spread between the Fair Market Value (FMV) on the exercise date and your exercise price was taxed as a perquisite — salary income — under Section 17(2)(vi) of the Income Tax Act. Your employer deducted TDS. That tax event is done.

The secondary sale is the second and final stage: capital gains on the difference between your sale price and the FMV on the exercise date (which is your cost of acquisition).

Stage | What's Taxed | Tax Type | Taxed When |

Exercise | FMV minus exercise price | Perquisite (Salary) | At exercise — TDS by employer |

Secondary Sale | Sale price minus FMV at exercise | Capital Gains | At sale — self-assessed / advance tax |

The cost of acquisition for your secondary sale is NOT your exercise price. It is the FMV on the exercise date. This is one of the most common — and costly — errors in secondary sale tax planning.

Capital Gains Tax Rates on Secondary ESOP Sales (FY 2025-26)

Since the shares are of an unlisted Indian company, the capital gains rules for unlisted shares apply. These were materially updated by the Finance Act, 2024, effective from 23 July 2024.

Holding Period (from exercise date) | Classification | Tax Rate |

24 months or less | Short-Term Capital Gains (STCG) | Applicable income tax slab rate (up to 30% + surcharge + cess) |

More than 24 months | Long-Term Capital Gains (LTCG) | 12.5% without indexation |

Key change from Budget 2024: The LTCG rate for unlisted shares was reduced from 20% (with indexation) to 12.5% without indexation for transfers on or after 23 July 2024. For most employees who acquired shares at relatively low FMV values and are selling at significantly higher prices, the flat 12.5% rate with no indexation is more favourable than the old 20% + indexation regime.

For most secondary sale scenarios at well-funded startups — where FMV has grown substantially since exercise — holding beyond the 24-month threshold is one of the highest-value tax planning decisions an ESOP employee can make. The difference between slab rate (up to 39%+ including surcharge) and 12.5% LTCG on a large secondary sale gain can be several lakhs or more.

Worked Example: Secondary Sale with LTCG vs STCG

Facts:

Exercise price: ₹50 per share

FMV on exercise date: ₹300 per share (perquisite already taxed at this point)

Secondary sale price: ₹800 per share

Shares sold: 5,000

Employee's income tax slab: 30%

Cost of acquisition for capital gains = ₹300 (FMV at exercise)

Capital gain = (₹800 − ₹300) × 5,000 = ₹25,00,000

Scenario | Rate | Tax Payable |

Held ≤ 24 months (STCG) | 30% slab + 4% cess | ~₹7,80,000 |

Held > 24 months (LTCG) | 12.5% + 4% cess | ~₹3,25,000 |

Tax saving from waiting past the 24-month threshold = ~₹4,55,000 on this single transaction. If you are approaching the 24-month mark on your exercise date, delaying the secondary sale — even by a few weeks — can be worth this difference in cash.

Holding Period: Counting It Correctly

The holding period for capital gains classification starts on the date of allotment of shares — i.e., the exercise date on which shares were actually transferred to your demat or folio. Not the grant date. Not the vesting date.

This matters in practice because many employees confuse the grant date (when they received the option) with the date from which the holding period runs. A grant issued in 2021 with a 4-year vesting schedule and exercise in 2024 starts its holding period clock in 2024 — not 2021.

To confirm your exact exercise (allotment) date: Check your allotment letter from the company, your SH-6 entry, or your depository statement showing the credit of shares.

Advance Tax Obligations on Secondary Sale Gains

This is where ESOP employees are most frequently caught off guard.

Capital gains from a secondary sale are not covered by employer TDS. The employer deducted TDS only on the exercise-stage perquisite. Capital gains are your personal liability — and they must be paid as advance tax in the financial year the sale occurs, not when you file your ITR.

Advance tax instalments for FY 2025-26:

Due Date | Minimum Cumulative Payment |

15 June 2025 | 15% of total estimated tax |

15 September 2025 | 45% of total estimated tax |

15 December 2025 | 75% of total estimated tax |

15 March 2026 | 100% of total estimated tax |

If a secondary sale closes in, say, August 2025, the capital gains from that sale become part of your estimated income for FY 2025-26. You should have included 45% of the estimated capital gains tax in your September 2025 instalment. Missing or underpaying advance tax attracts interest under Section 234B (1% per month on shortfall) and Section 234C (1% per month on instalment shortfall).

For large secondary sales where capital gains run into tens of lakhs, this interest can add up to a material amount. Do not wait until the ITR filing deadline to think about this.

FEMA Compliance for Secondary Transactions

If your ESOP shares are in an Indian company and the buyer is a non-resident — for example, a foreign VC or an overseas secondary market buyer — the transaction has FEMA implications.

Under FEMA 1999 and the Foreign Exchange Management (Non-debt Instruments) Rules, 2019, the transfer of shares of an Indian company to a non-resident must:

Be priced at or above the FMV as determined by a SEBI-registered Merchant Banker or under a specified valuation method (DCF or NAV)

Be reported in Form FC-TRS (Foreign Currency Transfer of Shares) with the Authorised Dealer Bank within 60 days of the transfer

Not violate sector-specific FDI caps applicable to the company

If you are selling through a company-facilitated window, the company should handle FEMA compliance. But if you are selling directly to a non-resident buyer on an individual basis, you — as the transferor — are jointly responsible for ensuring FC-TRS is filed. Non-compliance attracts compounding penalties under FEMA.

For resident-to-resident secondary sales, FEMA compliance is not required, but documentation of the transaction (sale agreement, consideration received, bank trail) should be maintained.

Tax Planning Strategies for Secondary ESOP Sales

1. Wait past the 24-month holding period if you can

As shown above, the tax difference between STCG (slab rate) and LTCG (12.5%) on a ₹25 lakh gain is over ₹4.5 lakh. If your exercise date puts you close to the 24-month mark, and the secondary transaction timeline is flexible, negotiate the closing date accordingly. Even a 30-day delay can shift an entire secondary sale to LTCG treatment.

2. Sell in a lower-income year

STCG on unlisted shares is taxed at your slab rate. If you have lower total income in a specific year — due to a career change, sabbatical, or reduced salary — executing the secondary sale in that year reduces the effective STCG rate. This requires advance planning coordinated with the liquidity window timeline.

3. Use Section 54F for LTCG reinvestment

If your secondary sale qualifies as LTCG (held > 24 months), the gain can be reinvested in a residential property under Section 54F to defer or reduce the LTCG tax liability. Conditions apply: you must not own more than one residential property at the time of sale, and the purchase/construction must occur within the specified window. This is a legitimate and widely used strategy — but requires professional planning before the sale closes, not after.

4. Budget for advance tax immediately after the transaction closes

As soon as a secondary sale closes, calculate your estimated capital gains and make advance tax payments on schedule. Do not treat the proceeds as fully yours before accounting for tax. Setting aside 15–20% of the net gain (above ₹1.25 lakh) immediately for tax payments protects you from the interest and penalty scenario.

5. Match exercise and sale dates deliberately

If you have un-exercised vested options and know a secondary window is coming, time your exercise date to maximise the holding period before the next expected liquidity event. Exercising today to sell in a secondary transaction 25 months from now qualifies for LTCG — exercising the day before a tender offer does not.

ITR Reporting for Secondary ESOP Sales

Secondary sale capital gains must be reported in your Income Tax Return under Schedule CG (Capital Gains). Key details to report:

Cost of acquisition: FMV on the exercise (allotment) date — obtain this from your employer's valuation report or grant documentation

Sale consideration: The gross amount received from the secondary buyer

Date of acquisition: The date of share allotment at exercise

Date of transfer: The date the secondary sale completed (share transfer date, not payment date)

Nature of gain: STCG or LTCG based on the 24-month threshold

If you received the secondary proceeds through a foreign account (for cross-border ESOP structures), you must also complete Schedule FA (Foreign Assets) disclosure. Missing Schedule FA is one of the most common and serious compliance gaps for employees receiving foreign parent employee share option plan benefits.

How Accorp Partners Helps With Secondary ESOP Sale Planning

Accorp Partners provides ESOP compliance and tax planning support to employees of Indian and cross-border ESOP companies — including secondary sale structuring, advance tax calculation, FEMA compliance, and ITR filing.

Our ESOP employee services include:

Secondary sale tax modelling — capital gains calculation, STCG vs LTCG analysis, advance tax schedules

Section 54F planning — structuring LTCG reinvestment in residential property to reduce capital gains liability

FMV documentation — obtaining and validating exercise-date FMV for cost of acquisition records

FEMA FC-TRS compliance — filing and documentation for secondary sales to non-resident buyers

ITR filing with ESOP disclosure — Schedule CG, Schedule FA, Form 67 (for foreign tax credit where applicable)

End-to-end ESOP scheme compliance — from scheme setup through secondary liquidity, we handle the complexity

Whether you are navigating your first secondary liquidity event or managing a large block sale at a pre-IPO company, understanding your tax position before the transaction closes — not after — is what separates a wealth-building employee stock ownership plan from an unexpected tax crisis.

Consult Accorp Partners to structure transparent, compliant, and high-impact ESOP plans that benefit both companies and employees.

Frequently Asked Questions

Q: How is a secondary ESOP sale taxed in India?

As capital gains. The gain is calculated as the sale price minus the FMV at the exercise date (cost of acquisition). If the shares were held for more than 24 months from the exercise date, it qualifies as LTCG at 12.5%. If held for 24 months or less, it is STCG taxed at your income tax slab rate.

Q: What is the cost of acquisition for secondary ESOP shares?

The FMV on the exercise date — not the exercise price you paid. The exercise price vs FMV spread was already taxed as a perquisite at exercise. Using the exercise price as the cost base would result in double taxation.

Q: What is the holding period for LTCG on secondary ESOP sales?

For unlisted Indian company shares, you must hold for more than 24 months from the date of allotment (exercise date). Selling within 24 months results in STCG at the slab rate. Holding beyond 24 months qualifies for the 12.5% LTCG rate.