Can Your Company Claim a Tax Deduction on ESOPs? Here's What the Law Says

Section 37(1) allows companies to claim ESOP tax deductions. Explore court rulings, compliance rules, and deduction timing.

Accorp Compliance Team

Our team of compliance experts specializes in PCI DSS, SOC 2, and other security frameworks to help businesses achieve and maintain compliance.

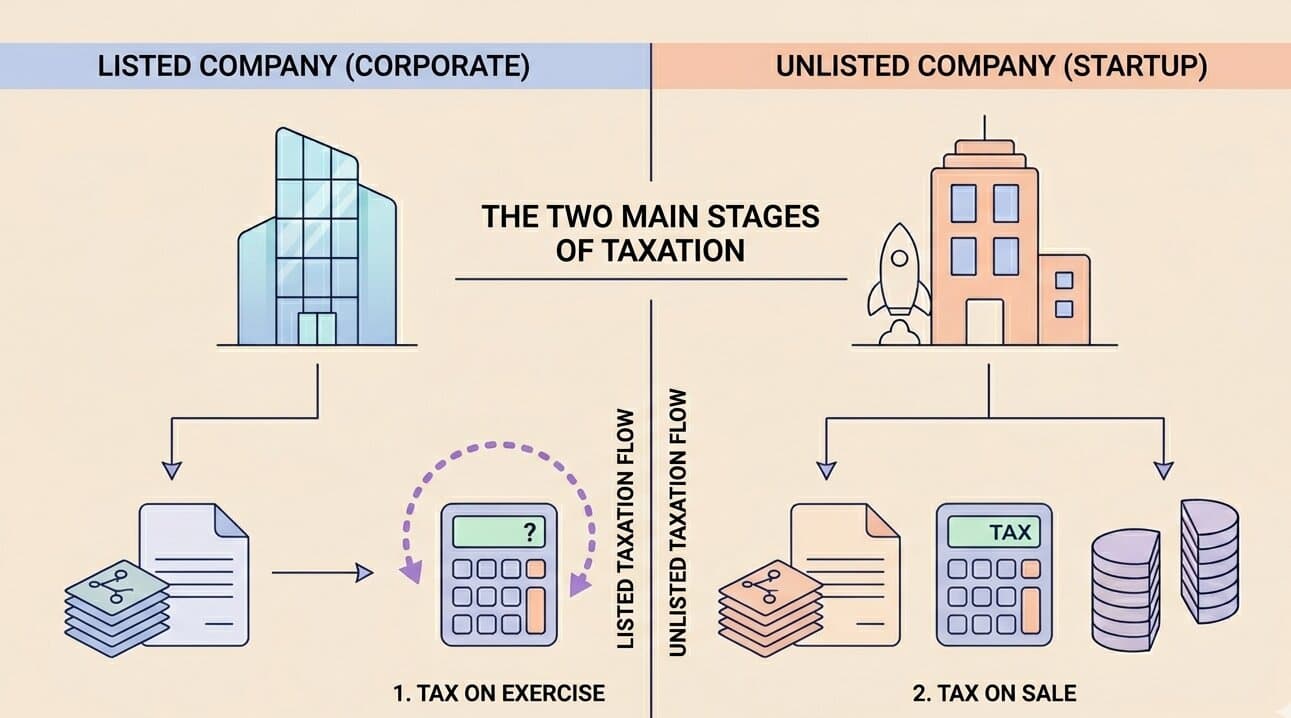

Every founder and CFO of an ESOP company knows that the employee stock option plan has a cost. You issue shares at below-market prices. You carry an Ind AS 102 expense on your books. You process TDS at exercise. But does any of this generate an actual income tax deduction for the company?

The answer is yes — but it has been anything but straightforward. The question of whether a company can claim a tax deduction on its ESOP scheme expenses has been one of the most litigated issues in Indian corporate tax law over the last two decades. The Income Tax Department routinely disallowed these claims on the grounds that the discount on ESOP stock is a "notional" or "capital" expense — not a real revenue expenditure.

Courts disagreed. Repeatedly.

This guide explains exactly what the law says, what the landmark rulings established, when and how your company can claim the deduction, and what you need to have in place from a compliance perspective to defend it.

The Core Question: Is ESOP Expense Revenue or Capital in Nature?

When a company grants stock options for employees under an employee share option plan, the financial cost to the company is the discount — the difference between the market price of the shares and the lower exercise price at which employees receive them. This discount represents real value transferred from the company to its employees as compensation for their continued service.

The Indian Income Tax Department's historical position was that this discount is:

Capital expenditure (because it involves shares — a capital asset), or

Notional (because no cash actually leaves the company), or

Contingent (because the employee might never exercise the options)

All three of these arguments have been categorically rejected by the courts. The settled legal position today is that ESOP expenses are allowable as revenue expenditure under Section 37(1) of the Income Tax Act, 1961.

What Section 37(1) Says

Section 37(1) is the residuary deduction provision of the Income Tax Act. It allows a deduction for any expenditure:

That is not personal in nature

That is not capital in nature

That is not covered under Sections 30 to 36

That is incurred wholly and exclusively for the purposes of the business

There is no specific section in the Income Tax Act that explicitly addresses the deductibility of employee stock option scheme expenses. Section 37(1) is the only provision under which companies can claim this deduction — and the courts have consistently held that it qualifies.

The primary legal basis: the purpose of an ESOP plan is to compensate employees and secure their continued service — an unambiguous revenue objective. It is not issued to create a capital asset. The cost is an employee cost, equivalent to salary or bonus, and should be treated identically for deduction purposes.

Landmark Court Rulings That Settled the Law

1. Biocon Ltd. vs DCIT — Karnataka High Court (2020)

The most widely cited ruling on ESOP deductibility in India. The Karnataka High Court upheld the deductibility of ESOP discount expenses and made two critical findings:

The discount on employee stock ownership is an ascertained liability, not a contingent one. The obligation exists from the date the options are granted — the exercise is merely a quantification of that liability at a future date.

The primary purpose of issuing share options for employees at a discount is to compensate employees for their service — a revenue objective. It cannot be treated as capital expenditure.

The deduction is allowable over the vesting period, consistent with how the expense is recognised in the books under accounting standards.

This ruling resolved the long-standing ambiguity and became the anchor precedent for subsequent decisions.

2. CIT vs Lemon Tree Hotels Ltd. — Delhi High Court (2015)

The Delhi High Court allowed the ESOP deduction claimed by Lemon Tree Hotels, holding that ESOP expenses are a definite legal liability and must be debited as an expense under the mercantile system of accounting. The court rejected the Department's argument that the expense was notional because no cash left the company.

This ruling is significant because it established that employee share ownership costs do not need to involve a cash outflow to qualify as an allowable deduction under Section 37(1).

3. PVR Ltd. vs CIT — Delhi High Court (2022)

The Delhi High Court allowed PVR's deduction for the difference between the market price and the issue price of stock options for employees granted under its employee share option plan. The court held that the primary object of the scheme was not to waste capital but to earn profits by securing the consistent services of employees — and therefore the cost cannot be construed as a short receipt of capital.

4. Recent ITAT Delhi Rulings (2025–2026)

Multiple recent ITAT Delhi decisions have reaffirmed the Section 37(1) deduction for ESOP companies, including a January 2026 ruling that deleted a ₹93 lakh disallowance and confirmed that the pendency of an SLP before the Supreme Court does not dilute the binding effect of Delhi High Court precedents (Lemon Tree Hotels, Biocon) for assessees within those jurisdictions.

When Is the Deduction Allowed — Vesting or Exercise?

This is one of the most practically important questions for companies managing an employee stock option scheme, and the answer depends on which accounting standard you follow.

Under Ind AS 102 (Share-Based Payments)

Companies that report under Indian Accounting Standards (Ind AS) follow Ind AS 102, which requires that the fair value of ESOP stock granted to employees be recognised as an employee compensation expense, spread over the vesting period.

Under this standard, the company determines the fair value of options on the grant date (using a Black-Scholes or binomial model from an IBBI Registered Valuer or approved actuary) and amortises that fair value as a P&L charge across the vesting period — typically 4 years.

For tax purposes: Multiple rulings, including Biocon and Lemon Tree Hotels, have accepted that the deduction can be claimed in accordance with the vesting-period accounting treatment. The Karnataka High Court specifically accepted that the deduction over the vesting period was consistent with both accounting principles and the law.

Under ICAI Guidance Note (Indian GAAP)

Companies following traditional Indian GAAP (Schedule III) use the ICAI Guidance Note on Accounting for Share-Based Payments (2020 revision), which also prescribes recognition of the intrinsic value or fair value of employee stock ownership grants as an expense over the vesting period.

The Exercise-Year Approach

Some courts and assessees have argued that the deduction should be claimed in the year of exercise — when the actual discount is quantified and shares are allotted. The Supreme Court has not yet definitively resolved whether vesting-period amortisation or exercise-year recognition is the correct approach for tax purposes. Until there is a Supreme Court ruling, the majority of High Court precedents support the vesting-period deduction.

Practical implication: If your company follows Ind AS 102 and amortises the ESOP plan cost over vesting, claim the deduction annually over the vesting period. If you claim in the exercise year, be prepared to defend the timing with supporting arguments and valuation documentation.

What Qualifies as the "ESOP Expense" for Deduction Purposes

The deductible expense is the discount — the excess of FMV over the exercise price — which represents the economic cost of the employee ownership benefit.

For unlisted companies, FMV must be certified by an IBBI Registered Valuer using the Black-Scholes or DCF methodology. This ESOP valuation report is not only necessary for computing employee perquisite tax — it forms the basis of the company's tax deduction claim. A weak or missing valuation report is the first thing the Income Tax Department challenges during assessment.

The deductible amount per share = FMV on the relevant date (grant or exercise, depending on your approach) − Exercise price

Multiplied by the number of options granted/exercised — this gives the total ESOP expense that the company can claim as a revenue deduction under Section 37(1).

Cross-Charged ESOP Expenses from Foreign Parent Companies

A specific and increasingly common situation: Indian subsidiaries of foreign companies receive employee share option plan grants from their parent (e.g., US, UK, or Singapore parent). The parent company issues the shares, and cross-charges the Indian subsidiary for the fair value of the options.

The ITAT has consistently held that cross-charged ESOP expenses are also allowable under Section 37(1), provided:

The cross-charge is supported by an inter-company agreement

The amount is quantified based on actual options exercised (not just the accounting amortisation)

The Indian subsidiary can demonstrate that the expense was incurred for business purposes — i.e., to retain employees working for the Indian entity

Merely recording the Ind AS 102 accounting charge without receiving an invoice from the parent is not sufficient. The claim should be based on actual cross-charges received for options actually exercised, supported by the parent's FMV documentation.

What the Department Still Challenges — And How to Defend Your Claim

Despite settled law in most High Courts, the Income Tax Department continues to disallow ESOP expenses at the assessment stage in many cases, particularly for:

Unlisted companies where FMV is not independently certified

Vesting-period claims where the Department argues deduction should only arise at exercise

Cross-charged parent ESOP expenses where documentation is incomplete

Amounts that differ between the P&L Ind AS 102 charge and the actual exercise-based deduction

To defend your Section 37(1) ESOP claim:

Maintain a certified FMV valuation report — dated, IBBI Registered Valuer or Merchant Banker signed, within 180 days of the relevant date

Document the scheme properly — a valid employee stock option scheme under the Companies Act (Board resolution, MGT-14 filed, SH-6 maintained)

Reconcile your P&L charge with your tax deduction — and keep a working that shows the methodology (vesting-period or exercise-year)

Keep grant letters and exercise records — the Department will verify that options actually vested and were exercised by employees on the payroll

For cross-charged expenses — maintain inter-company agreements and actual invoices from the parent company

Worked Example

A startup with an employee stock ownership plan makes the following grants in FY 2024-25:

Grant date FMV (unlisted): ₹200 per share (Registered Valuer certified)

Exercise price: ₹10 per share

Options granted: 50,000 shares over 4-year vesting

Total ESOP discount = (₹200 − ₹10) × 50,000 = ₹95,00,000

Under Ind AS 102, this ₹95 lakh is amortised over 4 years — ₹23.75 lakh per year as a P&L charge.

Tax deduction (vesting-period approach): ₹23,75,000 per year for 4 years under Section 37(1).

If the company claims this correctly with supporting FMV reports, scheme documentation, and consistent year-on-year treatment, the cumulative tax saving over 4 years at 25.17% (base corporate tax rate) is approximately ₹5.97 lakh — a meaningful benefit that many ESOP companies leave on the table by not asserting the deduction.

How Accorp Partners Helps With ESOP Deduction Claims

Accorp Partners is a CPA (USA) and CA (India) firm that provides end-to-end ESOP scheme compliance for Indian companies — including structuring the Section 37(1) deduction claim correctly.

Our ESOP services for companies include:

IBBI Registered Valuer FMV reports — Black-Scholes based, audit-ready, within valuation validity windows

Ind AS 102 workings — fair value determination, vesting-period amortisation schedules for auditors

ESOP scheme drafting and ROC filings — MGT-14, PAS-3, SH-6 maintenance under Companies Act, 2013

TDS compliance at exercise — perquisite computation, Form 24Q, Annexure II, Form 16 coordination

Section 37(1) deduction documentation — reconciliation of accounting charge vs tax claim, assessment defence support

Cross-border ESOP — inter-company charge structuring, FEMA compliance, FC-GPR reporting for parent-issued share options for employees

Whether you are setting up your first employee stock option plan or defending an ESOP deduction disallowance in assessment proceedings, we provide the expertise and documentation to support your position.

Consult Accorp Partners to structure transparent, compliant, and high-impact ESOP plans that benefit both companies and employees.

Frequently Asked Questions

Q: Can a company claim income tax deduction on ESOP expenses in India?

Yes. ESOP discount expenses are allowable as revenue expenditure under Section 37(1) of the Income Tax Act, 1961. This position is supported by multiple High Court rulings including Biocon (Karnataka HC, 2020), Lemon Tree Hotels (Delhi HC, 2015), and PVR Ltd. (Delhi HC, 2022).

Q: Is ESOP expense capital or revenue expenditure?

Revenue expenditure. Courts have held that the primary purpose of an employee stock option scheme is to compensate employees for their services — a revenue objective — and the cost cannot be treated as capital expenditure.

Q: When is the ESOP deduction allowed — at vesting or at exercise?

Under Ind AS 102, the fair value of options is amortised over the vesting period, and the courts have generally accepted the deduction on the same timing basis. Some assessees claim at exercise. The Supreme Court has not definitively settled this question. Most High Court precedents support the vesting-period approach.