The Complete ESOP Tax Guide: Grant, Vesting, Exercise & Sale — for Employees and Employers

ESOP tax rules for grant, vesting, exercise, and sale explained with TDS, capital gains, startup compliance, and filing details.

Accorp Compliance Team

Our team of compliance experts specializes in PCI DSS, SOC 2, and other security frameworks to help businesses achieve and maintain compliance.

If you have received an employee stock option plan grant from your employer, you are sitting on a potential financial benefit — but also a tax obligation that can surprise you if you are unprepared.

India's ESOP taxation framework is built on two separate taxable events, each governed by different sections of the Income Tax Act, different rates, and different obligations for both the employee and the employer. Most employees only discover how their employee stock ownership is taxed at the worst possible time: when TDS is deducted from their salary at exercise and their take-home drops to near zero for several months.

This guide covers every stage of the employee stock option scheme lifecycle — grant, vesting, exercise, and sale — with precise tax treatment, worked examples, and what employers must do to stay compliant. This is the guide you should read before you exercise a single share.

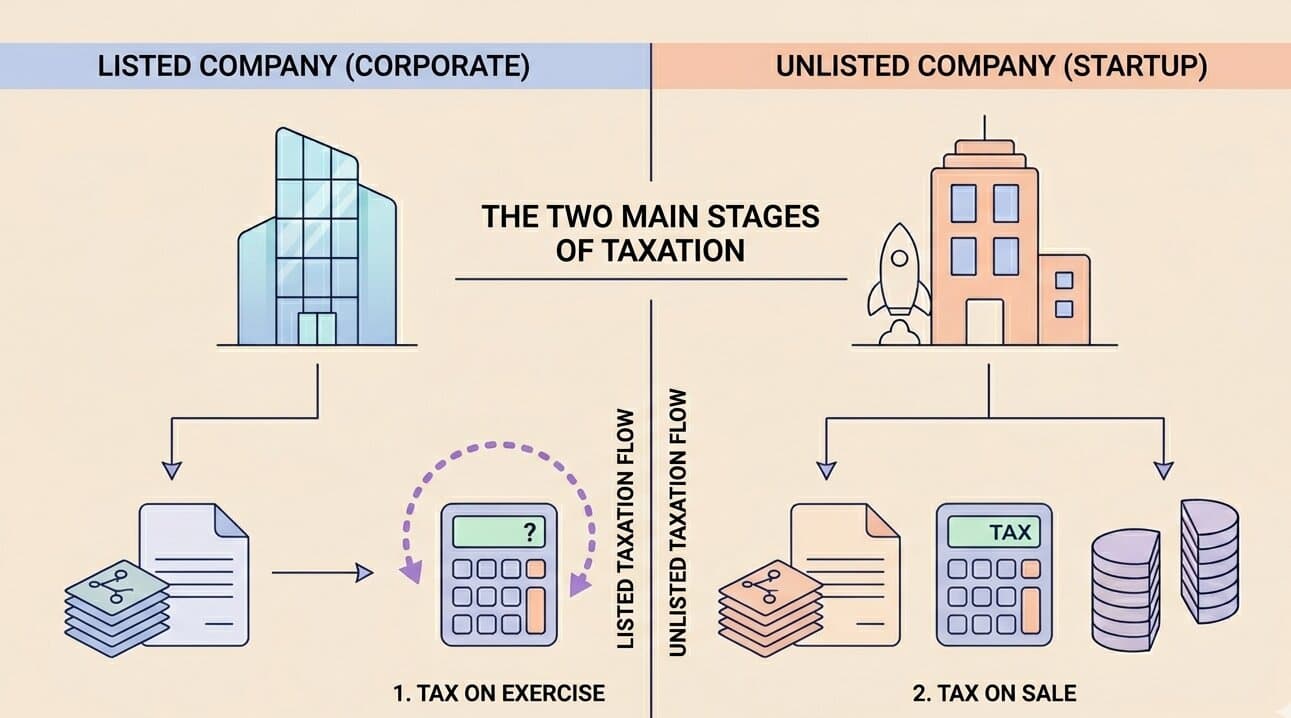

How ESOP Taxation Works: The Two-Stage Framework

The most important thing to understand about ESOP taxation in India is that it triggers at two distinct points — and each stage uses a different head of income, a different tax rate, and a different cost base.

The logic is deliberate. At exercise, the tax law treats the transaction as compensation from employer to employee — salary income. At sale, it treats the transaction as an investment gain — capital income. Each stage gets its own rules.

Stage 1 — Grant: No Tax

When your company grants you options under an employee share option plan, you receive a grant letter specifying the number of options, the exercise price (also called the strike price), and the vesting schedule. No money changes hands. No shares are allotted. No tax is triggered.

The grant is simply a contractual right to purchase shares at a future date and at a predetermined price. Until you actually exercise that right, there is no taxable event.

For employers: No tax obligation arises at grant. However, the grant must be documented with a board resolution, a shareholder-approved ESOP scheme, and a formal grant letter. Under the Companies Act, 2013, all employee stock option scheme grants must be covered by a scheme approved via special resolution and filed in Form MGT-14 with the Registrar of Companies.

Stage 2 — Vesting: Still No Tax

Vesting is the process by which your options become exercisable. A typical vesting schedule for an employee ownership plan is 4 years with a 1-year cliff: 25% of your options vest after 12 months, and the remaining 75% vest monthly or quarterly over the following 3 years.

Vesting itself creates no tax liability. You have not received shares. You have not paid anything. You have only earned the right to exercise. The tax clock does not start until you actually exercise.

Common vesting structures in ESOP companies:

Cliff vesting: A block vests on a specific date (e.g. 25% after Year 1)

Graded vesting: Equal tranches over 4 years (e.g. 25% per year)

Performance vesting: Vesting tied to company or individual KPIs

Acceleration: Some employee share ownership plan schemes include double-trigger acceleration at acquisition or IPO

For employers: No TDS, no payroll reporting, no ESOP valuation requirement at vesting. However, Ind AS 102 (Share-Based Payments) requires that the fair value of stock options for employees be recognised as an expense in the P&L, spread over the vesting period. This is an accounting obligation, not a tax obligation — but it affects your reported profitability and must be correctly computed by your auditors.

Stage 3 — Exercise: Perquisite Tax (The Stage That Catches People Off Guard)

This is the most consequential stage of the ESOP plan lifecycle for tax purposes. When you exercise your vested options, the company allots shares to you. The difference between the Fair Market Value (FMV) of those shares on the exercise date and the exercise price you paid is classified as a perquisite — a form of salary income — under Section 17(2)(vi) of the Income Tax Act, 1961.

How perquisite value is calculated

Perquisite value = (FMV on exercise date − Exercise price) × Number of shares exercised

How FMV is determined

Listed companies: FMV is the market price on the stock exchange on the exercise date (opening, closing, or average — per company policy)

Unlisted companies: FMV must be certified by a SEBI-registered Category I Merchant Banker (for income tax purposes) or an IBBI Registered Valuer using the Black-Scholes or DCF methodology. The valuation certificate must not be older than 180 days from the date of exercise. This is the ESOP valuation requirement that most early-stage startups overlook.

Worked Example — Unlisted Startup

Exercise price: ₹100 per share

FMV on exercise date: ₹500 per share

Shares exercised: 2,000

Perquisite = (₹500 − ₹100) × 2,000 = ₹8,00,000

This ₹8 lakh is added to your gross salary for FY 2025-26. If your other salary income is ₹15 lakh, your total taxable income becomes ₹23 lakh — attracting tax at the 30% slab on the higher portion.

The employee has not received cash. But the tax is real, immediate, and significant.

Employer TDS obligations at exercise

The employer is legally required to:

Calculate the perquisite value using certified FMV

Deduct TDS from the employee's salary under Section 192 of the Income Tax Act (Section 392 of the Income Tax Act, 2025) at the applicable slab rate

Deposit TDS by the 7th of the following month

Report the perquisite in Form 16 / Annexure II

File quarterly Form 24Q reflecting the perquisite income

Failure to deduct and deposit TDS makes the employer liable for interest under Section 201 and Section 220. ESOP-related TDS defaults are a common trigger for income tax scrutiny during audits of ESOP companies.

Section 80-IAC Deferral for Eligible Startups

If your employer is both DPIIT-recognised AND holds an IMB certificate under Section 80-IAC of the Income Tax Act (Section 140 under the Income Tax Act, 2025), the perquisite tax can be deferred to the earliest of:

48 months from the end of the assessment year of allotment

The date of sale of shares

The date of cessation of employment

This is a deferral, not an exemption. The tax is computed at slab rates applicable in the year of allotment — not the year of the trigger event. And if you resign before selling shares, the full tax falls due within 14 days of your last working day.

As of April 2026, only approximately 3,700 out of 1.97 lakh DPIIT-recognised startups have Section 80-IAC IMB certification. DPIIT recognition alone is not enough.

Stage 4 — Sale: Capital Gains Tax

When you eventually sell the shares you received at exercise, a second and separate taxable event occurs: capital gains tax. The FMV on the exercise date becomes your cost of acquisition for capital gains purposes — ensuring you are not taxed twice on the same gain.

Capital gain = Sale price − FMV on exercise date

Capital gains tax rates: FY 2025-26 (post Budget 2024 changes)

Share Type | Holding Period | Classification | Tax Rate |

Listed Indian shares (STT paid) | > 12 months | Long-Term (LTCG) | 12.5% above ₹1.25 lakh exemption |

Listed Indian shares (STT paid) | ≤ 12 months | Short-Term (STCG) | 20% |

Unlisted Indian shares | > 24 months | Long-Term (LTCG) | 12.5% without indexation |

Unlisted Indian shares | ≤ 24 months | Short-Term (STCG) | Applicable slab rate |

Worked Example — Sale at Unlisted Startup

Continuing from the earlier example:

FMV at exercise (cost of acquisition): ₹500 per share

Sale price (secondary sale, 26 months after exercise): ₹900 per share

Shares sold: 2,000

Holding period: 26 months > 24 months → LTCG

Capital gain = (₹900 − ₹500) × 2,000 = ₹8,00,000 LTCG tax @ 12.5% = ₹1,00,000

Compare this to paying the same gain as salary income at 30% slab: the difference between LTCG and slab treatment is ₹1,40,000 on this transaction alone. Timing the sale beyond the 24-month threshold for unlisted shares is a legitimate and significant tax planning decision.

ESOP Tax Summary: Employee vs Employer Obligations

Stage | Employee Obligation | Employer Obligation |

Grant | None | Draft scheme, file MGT-14, maintain SH-6 |

Vesting | None | Ind AS 102 expense recognition in P&L |

Exercise | Pay perquisite tax via TDS/self-assessment | Deduct TDS, file Form 24Q, issue Form 16 |

Sale | Pay capital gains, file ITR | No TDS obligation at sale (listed shares); report if required |

Key ESOP Tax Terms Every Employee Should Know

Exercise price / Strike price: The fixed price at which you can buy shares under your employee stock option plan — set at grant date FMV or below, per company policy.

Fair Market Value (FMV): The certified market value of the share on a specific date. For unlisted companies, this must come from an IBBI Registered Valuer or SEBI-registered Category I Merchant Banker. FMV drives both the perquisite calculation at exercise and the capital gains cost base at sale.

Vesting cliff: The minimum period you must remain employed before any options vest. Most ESOP schemes use a 1-year cliff — you receive nothing if you leave before 12 months.

ESOP buyback: Some unlisted ESOP companies offer buybacks before IPO or acquisition, allowing employees to sell shares back to the company or to a trust. Buyback proceeds are taxed as salary (not capital gains) in the hands of the employee, and TDS applies.

Lapse: Options that expire unexercised (typically 90 days after employment ends, per the scheme terms). Lapsed options return to the ESOP stock pool and can be regranted.

Common ESOP Tax Mistakes — Employees and Employers

Employee mistakes:

Not budgeting for TDS at exercise. At non-80-IAC companies, TDS is deducted from your salary the month you exercise. A large exercise can bring your take-home salary to near zero. Calculate the tax impact before exercising — especially if the perquisite is large relative to your monthly salary.

Using exercise price as capital gains cost. The cost of acquisition for capital gains is the FMV on exercise date, not what you paid. Using the exercise price double-taxes the perquisite gain. This is one of the most common ITR filing errors for ESOP employees.

Missing the LTCG holding period. For unlisted shares, selling even 1 day before 24 months converts LTCG (12.5%) to STCG (slab rate). Track your exercise date carefully.

Assuming DPIIT = automatic deferral. Only ~2% of DPIIT-recognised startups hold the IMB certificate under Section 80-IAC. Verify before assuming no TDS applies.

Employer mistakes:

No certified FMV at exercise. Granting or processing exercises without a valid Registered Valuer or Merchant Banker FMV report exposes the company to income tax scrutiny and potential TDS default penalties.

Missing Ind AS 102 accounting. For companies that have crossed the Ind AS threshold, failing to recognise share-based payment expense under Ind AS 102 misstates your financials — a significant issue at Series A and Series B due diligence.

Not filing PAS-3 at allotment. Every exercise that results in a share allotment requires a PAS-3 return of allotment filed with the ROC within 30 days. Many early-stage ESOP companies skip this, creating compliance gaps that surface during funding rounds.

ESOP scheme not updated after scheme expiry. Most employee stock option scheme documents have a 10-year validity. If the scheme has expired, all new grants are non-compliant. Review your scheme validity annually.

How Accorp Partners Helps With ESOP Tax and Compliance

At Accorp Partners, we are a CPA (USA) and CA (India) firm that handles end-to-end ESOP scheme compliance for Indian startups and established companies — from scheme drafting through exercise-stage TDS to Ind AS 102 audit workings.

Our ESOP services include:

ESOP scheme drafting — Companies Act, 2013 compliant scheme document, board and shareholder resolutions, grant letter templates

ROC filings — MGT-14, PAS-3 return of allotment, SH-6 register maintenance

IBBI Registered Valuer FMV reports — Black-Scholes methodology, audit-ready, within the 180-day validity requirement

TDS compliance at exercise — perquisite computation, Form 24Q, Annexure II, Form 16 coordination

Ind AS 102 share-based payment workings — expense recognition schedules, auditor-ready

Section 80-IAC eligibility review — verify DPIIT + IMB status before employees exercise to confirm deferral availability

ESOP buyback compliance — structuring buybacks correctly as salary vs capital gains

Cross-border ESOP compliance — FEMA, FC-GPR, RBI reporting for employees receiving parent-company stock options for employees

Fixed-fee pricing, no surprises. Whether you are setting up your first employee share ownership plan or resolving back-year exercise non-compliance, we handle the complexity.

Consult Accorp Partners to structure transparent, compliant, and high-impact ESOP plans that benefit both companies and employees.

Frequently Asked Questions

Q: Is ESOP taxable at grant in India?

No. There is no tax at the grant stage. Tax is triggered only at exercise (perquisite) and at sale (capital gains).

Q: Is ESOP taxable at vesting?

No. Vesting only means your options have become exercisable. No shares are allotted, no money changes hands, and no tax is due.

Q: When exactly is ESOP perquisite tax due?

At the time of exercise and share allotment. The employer deducts TDS in the month of exercise under Section 192 of the Income Tax Act.

Q: What is the cost of acquisition for capital gains when I sell my ESOP shares?

The FMV on the exercise date — not the exercise price you paid. This prevents double taxation of the perquisite gain.